Table of Content

You should talk to your insurance agent to determine the right amount — but as a general rule, your homeowners insurance should cover the full cost to replace your home. That means you should purchase coverage in a dollar amount equivalent to 100% of the cost of rebuilding your home from scratch. For example, if a hailstorm or the weight of snow after a blizzard damages your roof, a home insurance policy will likely pay for the repairs or a new roof. You don’t need to purchase a special type of insurance for roof replacement, but you can buy a home warranty that may help you with repairs not covered by homeowners insurance. So, what is dwelling coverage and what does homeowners insurance help cover?

A dwelling is an insured structure that is covered by dwelling insurance. For example, dwelling home insurance would cover the home itself, but not other structures on the property such as a shed or a fence. This is the preferable method of valuation for homeowners because it adds up how much it will cost to replace each of the lost structural features. Instead of your insurance paying out the value of your 10-year-old roof, for instance, you are paid for the amount to install a new roof of the same type. If there is doubt about what is and isn’t protected under dwelling coverage, ask your home insurance agent for clarification. Insurance companies are able to determine the amount of dwelling coverage based on factors such as square footage, garage type, number of fireplaces, and many other considerations.

What is Dwelling Coverage?

Martin Boonzaayer, CEO of The Trusted Home Buyer, makes an important observation about the current real estate market. With the advent of websites like Zillow.com, Redfin.com, and Realtor.com, even more data is available today than ever before. Many of these websites provide data like number of bedrooms, bathrooms, and garage spaces.

Coverage for damage to the structure caused by the same hazards as regular dwelling coverage. However, it often is possible to purchase separate insurance policies that cover these particular hazards. Dwelling coverage should be enough to cover the cost of rebuilding your home.

How Much Dwelling Coverage Do You Need to Protect Your Home?

O’Keefe says a licensed insurance agent can help advise you on whether extended dwelling coverage is right for your specific situation. “Extended dwelling coverage is designed to give wiggle room from the replacement cost coverage listed on your policy,” O’Keefe says. To calculate how much dwelling coverage you need, you first need to know how much it costs to rebuild.

NerdWallet strives to keep its information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product’s site. All financial products, shopping products and services are presented without warranty. When evaluating offers, please review the financial institution’s Terms and Conditions. If you find discrepancies with your credit score or information from your credit report, please contact TransUnion® directly. Your insurance agent can help you decide the type and amount of coverage you need.

How Much Dwelling Coverage Do I Need?

A homeowners insurance declaration page explains key facts about your homeowners insurance. Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers.

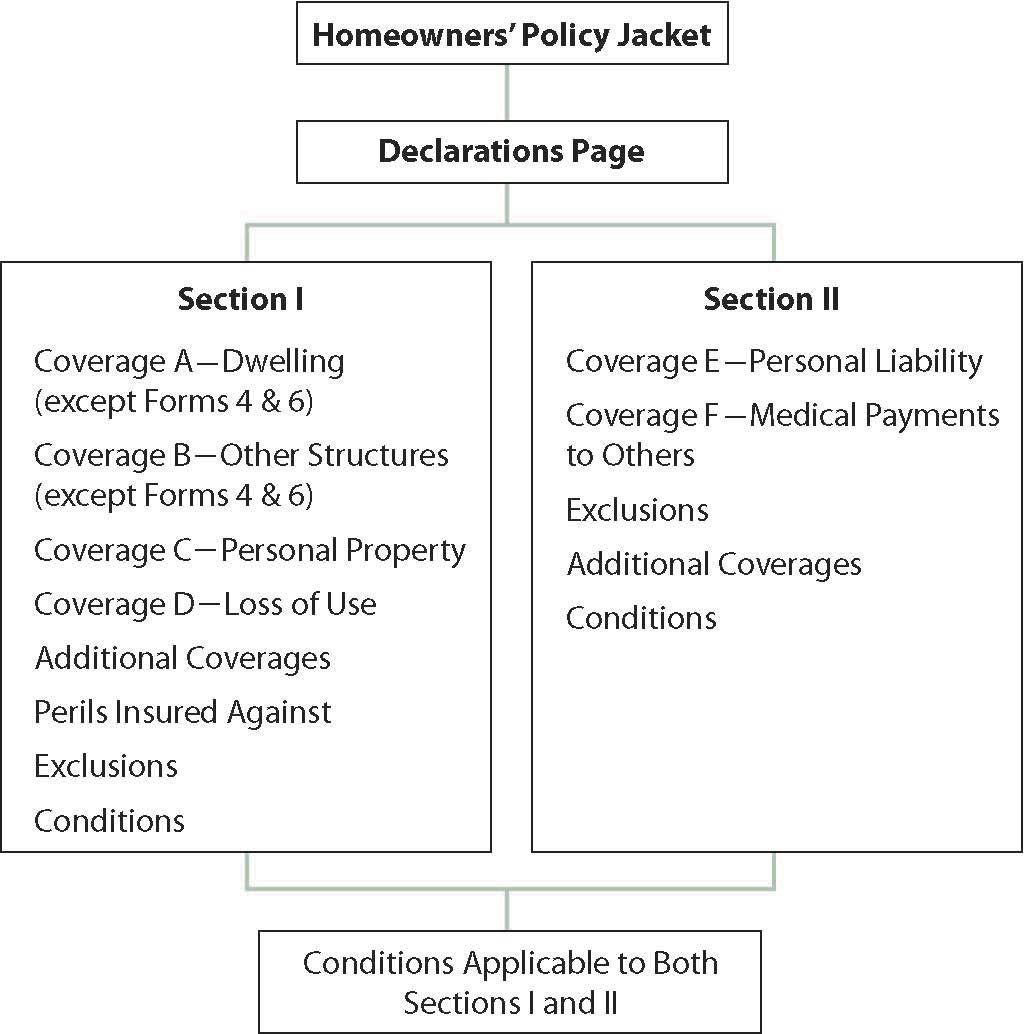

Guaranteed replacement cost coverage is generally the best, if you can find it. Guaranteed replacement cost is similar to extended replacement cost coverage, but it’s not capped at a certain percentage. Dwelling coverage is the part of a homeowners insurance policy that covers the physical structure of your home, including other structures on the property. Dwelling coverage refers to the coverage in your basic HO3 policy that covers your home, or in insurance lingo, dwelling.

Dwelling coverage is the part of homeowners insurance that covers damages to the physical structure of the policyholder’s home due to a covered peril. It provides protection against potentially significant expenses should it be necessary to rebuild the home. The right amount of coverage varies per person and will depend on individual needs. MoneyGeek breaks down what dwelling coverage is and how you can determine the amount of coverage suitable for you. Extended replacement cost coverage gives you some cushion when the cost to rebuild your house goes above your dwelling policy limits. This coverage can be particularly useful if your region is hit by a widespread disaster that causes a spike in local costs of materials and labor.

Once the claim has been settled and you receive your payout, you should hire a roofing company to fix the roof. The insurance company might provide a list of suggested contractors to work with, but you can hire any roofing company you want. Your roof acts as the primary defense against the elements and potential perils. For instance, a roof prevents water from pooling around the foundation, and it helps to regulate airflow in the attic through vents. Your roof needs to be structurally sound to avoid certain home insurance claims. Don’t assume that an HO-3 policy gives you complete coverage, though.

Custom homes have much higher replacement costs, based on the fact that it will take more materials, costlier materials plus the labor to rebuild them. On average, experts give us the estimate $200-$250 per square foot as the replacement cost of custom homes. Instead, you will have to purchase a separate flood insurance policy from an insurance provider or the National Flood Insurance Program . Your home insurance policy protects from personal liability so you aren’t responsible for damages and your insurance provider pays instead. Standard homeowners insurance, however, does not cover damage from floods or earthquakes. You’ll need separate policies for protection from these losses.

If you need more personal property coverage, you can typically buy more. You can choose the amount of your dwelling insurance deductible. The deductible is the amount that is deducted from your insurance check if you make a dwelling claim.

Make a separate inventory for these items, write down their estimated replacement costs, and ask your insurance agent if you need additional coverage for them. Homeowners insurance is a type of property insurance that safeguards your home and other valuable items. A standard policy covers damage and losses to your home and personal belongings. It also protects your assets from liability claims, such as personal injuries and pet-related incidents.

Not only do you pay a monthly fee, you typically pay a service fee each time a professional comes to your home. And if your roof is leaking due to age or wear and tear, you may need to replace the roof, which isn’t covered by a home warranty. You will likely have a deductible if your home insurance company approves a roof claim.

No comments:

Post a Comment